Personal Taxes & Support

Here is a brief wrap up of the 2020-21 Federal Budget as it relates to personal positions. We will see these changes come into place as legislation is passed.

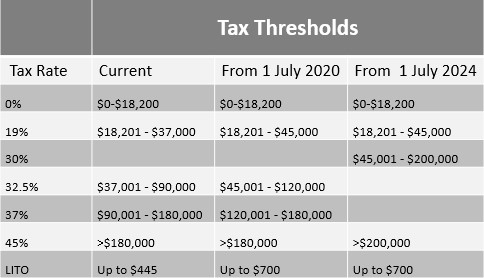

Tax cuts – Date of effect 1 July 2020

The Government has brought forward stage 2 of its planned income tax cuts by two years. Originally intended to apply from 1 July 2022, the tax cuts will come into effect from 1 July 2020 (subject to legislative requirements).

Stage 3 of the Personal Income Tax Plan remains scheduled for 2024-25.

Bringing forward the personal income tax plan will change thresholds as follows:

• Increase the top threshold of the 19% tax bracket to $45,000 (from $37,000)

• Increase the top threshold of the 32.5% tax bracket to $120,000 (from $90,000)

• Increase the low income tax offset from $445 to $700

In addition, the LMITO (low and middle income tax offset), which provides a reduction in tax of up to $1,080 for individuals with a taxable income of up to $126,000, will be retained for 2020-21. This measure was to be removed at the commencement of stage 2 of the reforms from 2022-23.

• Increase the top threshold of the 32.5% tax bracket to $120,000 (from $90,000)

• Increase the low income tax offset from $445 to $700

In addition, the LMITO (low and middle income tax offset), which provides a reduction in tax of up to $1,080 for individuals with a taxable income of up to $126,000, will be retained for 2020-21. This measure was to be removed at the commencement of stage 2 of the reforms from 2022-23.

Tax cuts – Date of effect 1 July 2020

Two additional economic support payments of $250 each will be made to eligible recipients of the following payments and health care card holders:

• Age Pension

• Disability Support Pension

• Carer Payment

• Family Tax Benefit, including Double Orphan Pension (not in receipt of a primary income support payment)

• Carer Allowance (not in receipt of a primary income support payment)

• Pensioner Concession Card (PCC) holders (not in receipt of a primary income support payment)

• Commonwealth Seniors Health Card holders

• Eligible Veterans’ Affairs payment recipients and concession card holders.

The payments are exempt from taxation and will not count as income support for the purposes of any income support payment.

• Disability Support Pension

• Carer Payment

• Family Tax Benefit, including Double Orphan Pension (not in receipt of a primary income support payment)

• Carer Allowance (not in receipt of a primary income support payment)

• Pensioner Concession Card (PCC) holders (not in receipt of a primary income support payment)

• Commonwealth Seniors Health Card holders

• Eligible Veterans’ Affairs payment recipients and concession card holders.

The payments are exempt from taxation and will not count as income support for the purposes of any income support payment.

Other Personal Support

Subject to the passing of legislation, other support was announced:

• Removing Capital Gains Tax for Granny Flats – Date of Effect 1 July 2021

• 10,000 additional places in First Home Loan Deposit Scheme – Date of effect 6 October 2020 until 30 June 2021. This supports the purchase of a new home or a newly built home. The scheme enables first home buyers to purchase a home with a deposit of as little as 5% without mortgage insurance across 27 participating lenders

• $1.6bn to help elderly stay at home over 4 years from 2020-21 to release an additional 23,000 home care packages across all package levels.

• Aged care industry monitoring and support through an additional $400 million including a new serious incident response scheme and monitoring services.

• Superannuation – steps and processes to prevent duplication of super accounts Date of effect from 1 July 2021.

• Superannuation – accountability of underperforming funds – Date of effect From July 2021 in relation to MySuper products and from 1 July 2022 for non MySuper products through programs and testing by Australian Prudential Regulation Authority and greater transparency of MySuper information (through tools provided by the ATO).

• Superannuation – Trustee accountability – Date of effect by 1 July 2021. Superannuation trustees will be required to comply with a new duty to act in the best financial interests of members and must demonstrate that there was a reasonable basis to support their actions being consistent with members’ best financial interests including providing key information and how they manage finances in advance of Annual Members’ Meetings.

• 10,000 additional places in First Home Loan Deposit Scheme – Date of effect 6 October 2020 until 30 June 2021. This supports the purchase of a new home or a newly built home. The scheme enables first home buyers to purchase a home with a deposit of as little as 5% without mortgage insurance across 27 participating lenders

• $1.6bn to help elderly stay at home over 4 years from 2020-21 to release an additional 23,000 home care packages across all package levels.

• Aged care industry monitoring and support through an additional $400 million including a new serious incident response scheme and monitoring services.

• Superannuation – steps and processes to prevent duplication of super accounts Date of effect from 1 July 2021.

• Superannuation – accountability of underperforming funds – Date of effect From July 2021 in relation to MySuper products and from 1 July 2022 for non MySuper products through programs and testing by Australian Prudential Regulation Authority and greater transparency of MySuper information (through tools provided by the ATO).

• Superannuation – Trustee accountability – Date of effect by 1 July 2021. Superannuation trustees will be required to comply with a new duty to act in the best financial interests of members and must demonstrate that there was a reasonable basis to support their actions being consistent with members’ best financial interests including providing key information and how they manage finances in advance of Annual Members’ Meetings.

• Aged care industry monitoring and support through an additional $400 million including a new serious incident response scheme and monitoring services.

• Superannuation – steps and processes to prevent duplication of super accounts Date of effect from 1 July 2021.

• Superannuation – accountability of underperforming funds – Date of effect From July 2021 in relation to MySuper products and from 1 July 2022 for non MySuper products through programs and testing by Australian Prudential Regulation Authority and greater transparency of MySuper information (through tools provided by the ATO).

• Superannuation – Trustee accountability – Date of effect by 1 July 2021. Superannuation trustees will be required to comply with a new duty to act in the best financial interests of members and must demonstrate that there was a reasonable basis to support their actions being consistent with members’ best financial interests including providing key information and how they manage finances in advance of Annual Members’ Meetings.

• Superannuation – accountability of underperforming funds – Date of effect From July 2021 in relation to MySuper products and from 1 July 2022 for non MySuper products through programs and testing by Australian Prudential Regulation Authority and greater transparency of MySuper information (through tools provided by the ATO).

• Superannuation – Trustee accountability – Date of effect by 1 July 2021. Superannuation trustees will be required to comply with a new duty to act in the best financial interests of members and must demonstrate that there was a reasonable basis to support their actions being consistent with members’ best financial interests including providing key information and how they manage finances in advance of Annual Members’ Meetings.

Business Support

Further initiatives and announcements may support small business and economic activity, including:

• A $4 billion ‘JobMaker’ Hiring Credit to encourage businesses to take on additional employees aged 16 to 35 years old

• Immediate deductions for business investment in capital assets

• Access to further tax concessions for a wider range of businesses

• $110 billion in infrastructure investment over 10 years

• Immediate deductions for business investment in capital assets

• Access to further tax concessions for a wider range of businesses

• $110 billion in infrastructure investment over 10 years

JobMaker Hiring Credit

The JobMaker Hiring Credit will be available to eligible employers over 12 months from 7 October 2020 for each additional new job they create for an eligible employee.

Eligible employers will receive:

– $200 per week if they hire an eligible employee aged 16 to 29 years or

– $100 per week if they hire an eligible employee aged 30 to 35 years.

The JobMaker Hiring Credit will be paid quarterly in arrears. It will be available for up to 12 months from the date of employment of the eligible employee with a maximum amount of $10,400 per additional new position created.

Employers will need to demonstrate that the new employee will increase overall employee headcount and payroll.

To be eligible, the employee will need to have worked for a minimum of 20 hours per week, averaged over a quarter, and received the JobSeeker Payment, Youth Allowance (other) or Parenting Payment for at least one month out of the three months prior to when they are hired.

– $200 per week if they hire an eligible employee aged 16 to 29 years or

– $100 per week if they hire an eligible employee aged 30 to 35 years.

The JobMaker Hiring Credit will be paid quarterly in arrears. It will be available for up to 12 months from the date of employment of the eligible employee with a maximum amount of $10,400 per additional new position created.

Employers will need to demonstrate that the new employee will increase overall employee headcount and payroll.

To be eligible, the employee will need to have worked for a minimum of 20 hours per week, averaged over a quarter, and received the JobSeeker Payment, Youth Allowance (other) or Parenting Payment for at least one month out of the three months prior to when they are hired.

To be eligible, the employee will need to have worked for a minimum of 20 hours per week, averaged over a quarter, and received the JobSeeker Payment, Youth Allowance (other) or Parenting Payment for at least one month out of the three months prior to when they are hired.

From acquisition of eligible capital assets from 7:30pm AEDT on 6 October 2020 and first used or installed by 30 June 2022.

This enables businesses with an aggregated turnover of less than $5 billion to fully expense the cost of new depreciable assets and the cost of improvements to existing eligible assets in the first year of use. This means that an asset’s cost will be fully deductible (upfront rather than being claimed over the asset’s life) and is uncapped.

The existing $150,000 instant asset write-off applies to businesses with turnover less than $500 million and will not apply to purchases after 31 December 2020.

The existing $150,000 instant asset write-off applies to businesses with turnover less than $500 million and will not apply to purchases after 31 December 2020.

Second-hand assets

For businesses with an aggregated turnover under $50 million, full expensing also applies to second-hand assets.

Businesses with aggregated annual turnover between $50 million and $500 million can still deduct the full cost of eligible second-hand assets costing less than $150,000 that are purchased by 31 December 2020 under the existing enhanced instant asset write-off. Businesses that hold assets eligible for the enhanced $150,000 instant asset write-off will have an extra six months, until 30 June 2021, to first use or install those assets.

Small business pooling

Small business entities (with aggregated annual turnover of less than $10 million) using the simplified depreciation rules can deduct the balance of their simplified depreciation pool at the end of the income year while full expensing applies. The provisions which prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out will continue to be suspended.

Carry-back losses

Losses from the 2019-20, 2020-21 or 2021-22 income years.

Companies with an aggregated turnover of less than $5 billion will be able to carry back losses from the 2019-20, 2020-21 and 2021-22 income years to offset previously taxed profits in the 2018-19, 2019-20 and 2020-21 income years. Tax losses can be applied against taxed profits in a previous year, generating a refundable tax offset in the year in which the loss is made. The amount carried back can be no more than the earlier taxed profits, limiting the refund by the company’s tax liabilities in the profit years and the carry back cannot generate a franking account deficit meaning that the refund is further limited by the company’s franking account balance.

The tax refund will be available on election by eligible businesses when they lodge their 2020-21 and 2021-22 tax returns.

The tax refund will be available on election by eligible businesses when they lodge their 2020-21 and 2021-22 tax returns.

Research & Development

Date of effect 1 July 2021

Currently, the R&D Tax Incentive provides the following in respect of eligible R&D activities (for the first $100 million of eligible expenditure):

– a 43.5% refundable offset for eligible companies with aggregated annual turnover less than $20m; and

– a 38.5% non-refundable tax offset for all other eligible companies.

Note that the Treasury Laws Amendment (Research and Development Tax Incentive) Bill 2019 before Parliament at the time the Federal Budget was released, proposed various amendments to the R&D Tax Incentive to take effect from the 2019-20 income year. The Government is now delaying (by two years) and enhancing the proposed changes.

For companies with an aggregated annual turnover less than $20 million:

– The refundable R&D tax offset is being set at 18.5% above the claimant’s company tax rate (an increase from 13.5% above the claimant’s company tax rate as previously announced)

– The previously announced annual $4 million cap on cash refunds for R&D claimants will not proceed.

For companies with aggregated annual turnover of $20 million or more, the previously announced R&D intensity premium, originally intended to apply across three tiers, will now apply across two tiers.

The R&D expenditure threshold being the maximum amount of R&D expenditure eligible for concessional R&D tax offsets, will be increased as intended from $100 million to $150 million per annum.

– a 43.5% refundable offset for eligible companies with aggregated annual turnover less than $20m; and

– a 38.5% non-refundable tax offset for all other eligible companies.

Note that the Treasury Laws Amendment (Research and Development Tax Incentive) Bill 2019 before Parliament at the time the Federal Budget was released, proposed various amendments to the R&D Tax Incentive to take effect from the 2019-20 income year. The Government is now delaying (by two years) and enhancing the proposed changes.

For companies with an aggregated annual turnover less than $20 million:

– The refundable R&D tax offset is being set at 18.5% above the claimant’s company tax rate (an increase from 13.5% above the claimant’s company tax rate as previously announced)

– The previously announced annual $4 million cap on cash refunds for R&D claimants will not proceed.

For companies with aggregated annual turnover of $20 million or more, the previously announced R&D intensity premium, originally intended to apply across three tiers, will now apply across two tiers.

The R&D expenditure threshold being the maximum amount of R&D expenditure eligible for concessional R&D tax offsets, will be increased as intended from $100 million to $150 million per annum.

For companies with an aggregated annual turnover less than $20 million:

– The refundable R&D tax offset is being set at 18.5% above the claimant’s company tax rate (an increase from 13.5% above the claimant’s company tax rate as previously announced)

– The previously announced annual $4 million cap on cash refunds for R&D claimants will not proceed.

For companies with aggregated annual turnover of $20 million or more, the previously announced R&D intensity premium, originally intended to apply across three tiers, will now apply across two tiers.

The R&D expenditure threshold being the maximum amount of R&D expenditure eligible for concessional R&D tax offsets, will be increased as intended from $100 million to $150 million per annum.

– The previously announced annual $4 million cap on cash refunds for R&D claimants will not proceed.

For companies with aggregated annual turnover of $20 million or more, the previously announced R&D intensity premium, originally intended to apply across three tiers, will now apply across two tiers.

The R&D expenditure threshold being the maximum amount of R&D expenditure eligible for concessional R&D tax offsets, will be increased as intended from $100 million to $150 million per annum.

Access to tax concessions extended to businesses up to $50m

Three phases: 1 July 2020, 1 April 2021 and 1 July 2021

Announced pre Budget, a range of generous tax concessions normally only available to small and medium businesses, will be available to businesses with an aggregated turnover of up to $50 million.

The expanded concessions will be rolled out in three phases:

The expanded concessions will be rolled out in three phases:

The eligibility turnover thresholds for other small business tax concessions will remain at their current

FBT exemption for retraining and reskilling workers

Date of effect: 2 October 2020

Announced pre Budget, the Government will provide a Fringe Benefits Tax (FBT) exemption for employer provided retraining and reskilling, for employees who are redeployed to a different role in the business.

Currently, if an employer provides a benefit to an employee that is not directly related to their current job, FBT applies. This measure enables employers to help employees reskill for a new role or another role with a different employer, without incurring FBT.

The exemption does not apply to retraining acquired through salary packaging or training provided through Commonwealth supported places at universities. The exemption also does not extend to repayments towards Commonwealth student loans.

The Government will also consult on potential changes to the law to allow a worker to deduct expenses they personally incur to undertake training directed at future employment and skills (current rules that limit deductions to training related to current employment, may act as a disincentive for workers to retrain and reskill).

Currently, if an employer provides a benefit to an employee that is not directly related to their current job, FBT applies. This measure enables employers to help employees reskill for a new role or another role with a different employer, without incurring FBT.

The exemption does not apply to retraining acquired through salary packaging or training provided through Commonwealth supported places at universities. The exemption also does not extend to repayments towards Commonwealth student loans.

The Government will also consult on potential changes to the law to allow a worker to deduct expenses they personally incur to undertake training directed at future employment and skills (current rules that limit deductions to training related to current employment, may act as a disincentive for workers to retrain and reskill).

The Government will also consult on potential changes to the law to allow a worker to deduct expenses they personally incur to undertake training directed at future employment and skills (current rules that limit deductions to training related to current employment, may act as a disincentive for workers to retrain and reskill).

Other announcements include:

– Corporate residency test changes

– FBT record keeping simplified

– Managed investment trust withholding rate standardised across international information sharing agreements

– Victorian business support grants to be tax-free post 13/9/20

– 100,000 new apprenticeships

– Specific regional COVID-19 funding and natural disasters relief

If you require any further information or would like to discuss the above, please contact us.

This content is provided for general information purposes only and is not intended to constitute legal or other professional advice

Liability limited by a scheme approved under Professional Standards Legislation

Find Us On Social

![]()

![]()